Creating Value

Creating Value

Tokens within the spinning flywheel of time

Grounded

Too often projects are deploying short-term with unethical intentions. Perhaps morality should not be brought in to play in an industry where everyone is focused on making the next dollar. Regardless of what lens you choose to view this, it is important to arm yourself with the ability to screen out the ever increasing “ponzinomics” that seems to rile up our industry. Whilst I hold a neutral stance as a writer, I am of the belief that these scams have the potential to devastate the entire reputation of our industry, with few eventual winners.

Short term goals. Anonymous teams. Rugs. This sequential pattern has happened time and time again. A fourth missing step would be — repeat. There are those who wish to accrue as much capital as possible, and immediately. To reach these means, they will make it a mission to happily step over moral boundaries that act as a framework for our society as long as their pockets get fatter.

As adoption into the crypto atmosphere grows at an exponential rate, projects also are launching at an unrivalled speed. It is much harder to create long-term value for a project, than to rug.

It is well known that there is good amongst bad (amongst ugly). If you didn’t get the reference, I’m disappointed to say the least. Anyway, to start with most projects don’t even require a token, other than for fundraising initial capital.

The main reason the public would want to make such a trade is if the tokenomics behind a project follow sound math or economics. Which in turn allows the crypto to have more value or utility after network growth. Aligning long-term usage with the token is hard and requires complex understanding.

Simply phrased, it doesn’t matter how strong the project is. It loses its’ investment credentials as soon as the tokenomics become “bad”.

In the remainder of this article, I will formalize the tenets of tokenomics, their necessity and how they can be applied to launching projects. For investors, it is equally as important to be able to recognize where value accrues. Spotting it early, could lead to your best investment as of yet…

The Necessity of Tokens

Crypto tokens are a legal and unregulated way to fundraise capital for your crypto project in exchange for long term control of your project. Unlike traditional venture capital you can do this extremely independently, without requiring the SEC to get involved like a corporate startup venture might.

Many of the shadowy-teen super coders today don’t have the funds to launch a project. To do so, it will require basic variable costs such as staff, equipment etc. The allocation of cryptocurrency tokens is a way for founders to fundraise capital, often in exchange for control over the project in the form of governance.

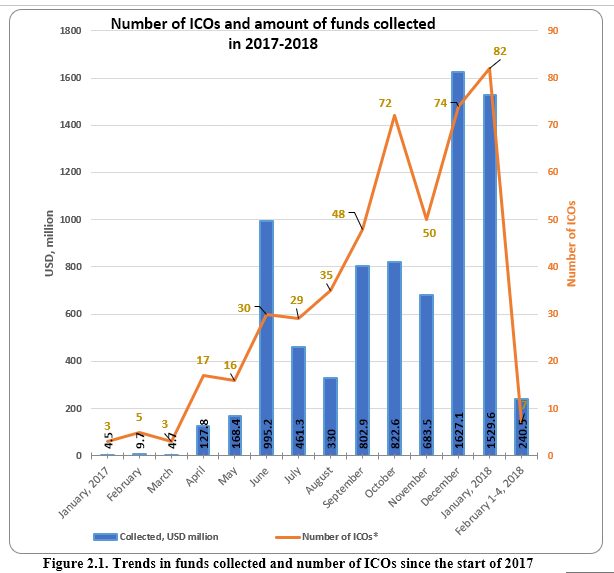

In the past, one of the most common forms of raising money for a project would be through initial coin offerings (ICOs).An ICO is the cryptocurrency industry’s equivalent to an initial public offering (IPO), which dominates the stock markets. ICO activity began to decrease dramatically in 2019, because of the high levels of risk that were eventually shown to the wider public.

Most projects these days will rely on Venture Capital (VC) firms as a way of raising the required amount of capital. With VC financing, businesses can often obtain large amounts of capital and with ease. A lot of companies are well networked, experienced and provide the opportunity to scale a project at a much faster rate, than what would have otherwise have been impossible.

Allocating Tokens

As a disclaimer, none of this is financial advice and should not be used as such. These are simply my thoughts…

When embarking on a project launch, it can be difficult to know how and to whom you allocate tokens too. Asymmetric distribution of tokens amongst members “in it for the short term” can lead to consequences such as dumping if protectionist mechanisms such as lock-ups aren’t in place.

There is a clear difference between equity in traditional finance markets and token allocation and thus they should be treated as separate entities. Traditional equity such as bonds, cash, real estate, and shares have arguably less use cases than tokens. This has been well explored here but for simplicity we will lay out the key differences.

Tokens tend to have:

Instant liquidity

Additional token bearing incentives: staking, lending and yield incentives

Transparency of dilution

Talent based rewards not limited by local/global regulations and institutional hierarchies

Prior to protocol launch it is important to decide how employees need to be rewarded. This can be done through equity, tokens or a mixture of both. Consulting with legal and crypto experts can be a useful way to create strategic plans.

As an investor, it is important to understand the distribution of tokens, lock-up periods and vesting schedules(cliff/linear). Token infrastructure and strategy is always up to the project founders, but you can always reach out to me here for further questions you may have.

Distribution of tokens: It is important to note that the majority of projects will have a fixed supply of tokens. In their documents there should be references to how they have been distributed amongst key holders, which usually are the team and early investors. Some tokens can be locked up for protocol-related functions such as liquidity mining. The rest is usually what is termed as “the circulating supply”. I would recommend checking this before any investment. If the distribution leans too heavily in favor of one party, this is generally considered as a red flag.

Lock-up Periods: Upon launch of a project many of the early stage investors and team will be subject to a lock-up period. This is where they will not be able to sell their tokens until an agreed date. Longer term lockups tend to gain greater trust from the community.

Cliffs/linear vesting: Linear vesting is the most common, where a recurring percentage is unlocked over a period of time. A cliff is where they become fully vested on a specific date- all tokens unlock at once. Perhaps a more efficient vesting strategy would be back-weighted strategy where employees vest a larger percentage each year. This incentivizes longer term retention in the project; Year one: 5%; Year two: 20%; Year three: 40% etc.

My withstanding thesis is as follows. There is information asymmetry everywhere, specifically with lock-up schedules. Average investors are not aware of most lock-up period dates and this can impact their investment if the token dumps. From a moral constraint (and perhaps as this space moves forward) more back-weighted strategies applied incrementally i.e small token unlocks every four hour period would mean there won’t be sudden unregisterable shocks in selling pressure. This would have to be addressed by smarter people than me, however.

Value

Tokens are not equity and therefore should not be treated as such. More importantly, they shouldn’t be issued for the sake of doing them. Take Optimism or Arbitrum, for example. There is no actual benefit to the community or protocol by issuing a token.

When project founders issue a token it bears:

Reputation risk

Financial risk

Legal risk

/ Twitter")

It is important to conduct a cost/benefit analysis and determine whether it is necessary to deploy a token. But if the token is deployed, as investors we need a framework to determine where value accrual lies:

Governance: By owning the token do you get a share of the governance over the protocol. How much governance do your receive? Is the amount of governance subject to change? What are the percentages of token allocation among whales? How much governance is required to pass a proposal?

Ownership: By owning the token do you have ownership over something? A fractionalized NFT? A DAO? Gated communities? Do you stand to gain monetarily from this ownership? Can create a new product with token? Token for storage/gas fees- what is the core utility?

Supply: Is there a fixed supply? What is the mechanism for how the illiquid supply is distributed e.g PoW? Are tokens inflationary (more being printed than burnt) or deflationary?

Profits: Does your blockchain autonomously distribute profits/benefits to token holders?

Determining where value lies is arguably as important as the technology behind it- unless your an extreme maximalist. If project founders can incentivise value in the token by aligning the incentives of the protocol with that of long term holders, it is a sure pathway to success. We will explore this later in the form of network effects and flywheels…

Adaptable Tokenomics

When prices are high, people will often forget to re-evaluate their investments that they planned to hold for the longer term. It is important to distinguish between intrinsic and speculative value:

Intrinsic value- The value the token gains from the credibility and utility of its project.

Speculative Value- The value the token gains from speculations traders make on a tokens price.

Often people will omit that there has to be an intrinsic value in the token. By first principles, it is safe for me to invest when the value of the token is less than the intrinsic value.

Imagine it in terms of collateral. Each token X is backed by 15$ worth of equipment and 5$ of data storage tokens.

Therefore token X is at least backed by 20$.

Unfortunately, in a market where speculation is high, it is only possible to make relative judgements and in an ordinal manner. Judgements like these will always be subjective. However, understanding the value in the token and making such a judgement- allows me to have confidence in my investment.

Network effects

To truly understand how growth compounds, its’ fundamental to understand network effects. Network effects essentially is where the network becomes increasingly valuable to the user as more people use it. At its core, Metcalfe’s Law implies that platforms and products with network effects get better as they get bigger. They improve both in value to users, but also in accruing more resources to improve their product, creating a flywheel of sorts.

If you are investing in a project with strong network effects, it is likely that you will see increased value coming in. In the traditional markets an example of network effects would be how Youtube has created “shorts” in a manouevre to corner the market share of Tiktok. In the crypto world however, network effects can be accentuated by grants.

When a grant fund is introduced, I refer back to these three principles and see whether it impacts my underlying confidence in an investment:

Value (e.g token): What drives price increases in token? When does diminishing marginal utility kick in? Does value increase from the ecosystem accelerating?

Users/inventory: Commoditized/Differentiated? Greater adoption flywheels?

Ecosystem: Network overlap? Cost reductions? More dApps being built?

Is important to remain ahead of competitors by being dynamic in utilising network effects.

My thesis would be that as there become clear differentiators in the field, eg like Ethereum in layer 1, there will be a greater emphasis on utilising network effects to remain ahead of the competition.

Network effects only comes with growth however. We haven’t seen games being delivered on the same size as Fortnite. Within the GameFi industry for example, there should be greater focus on delivering the product and maintaining basic demand and supply imbalances,than the implementation of network effects.

Positive Flywheels

By definition, a blockchain that is designed correctly cannot benefit from any kind of scarce resource due to its open and permissionless nature. The very notion that a blockchain is decentralized means that there exists no small group of people that has unilateral control or outsized power over it; everyone plays on the same level playing field.

So how does one go about capturing value?

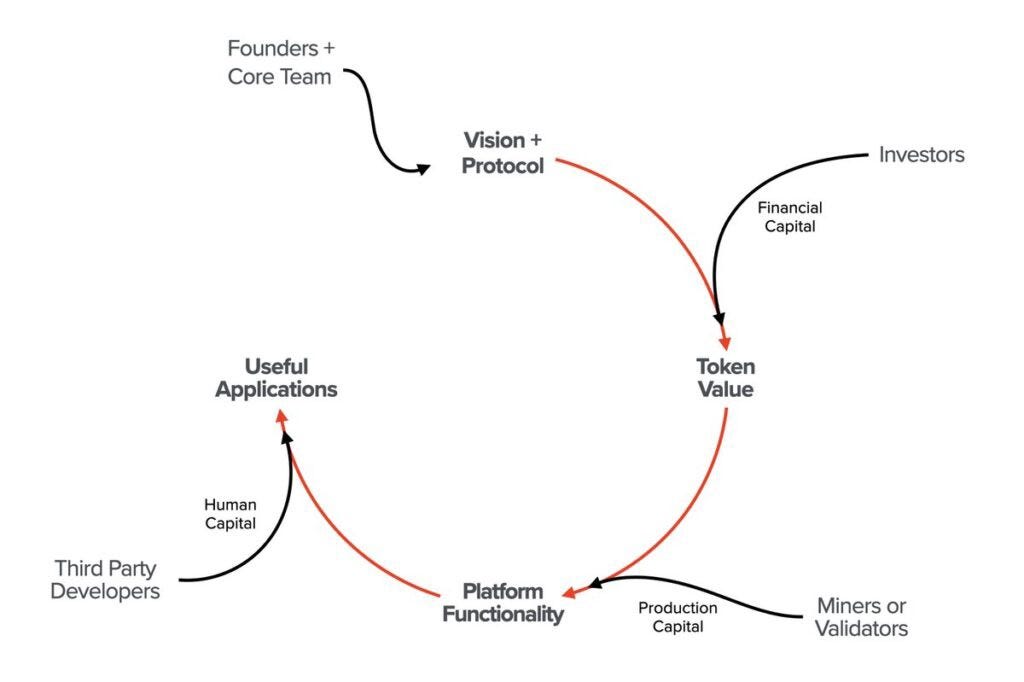

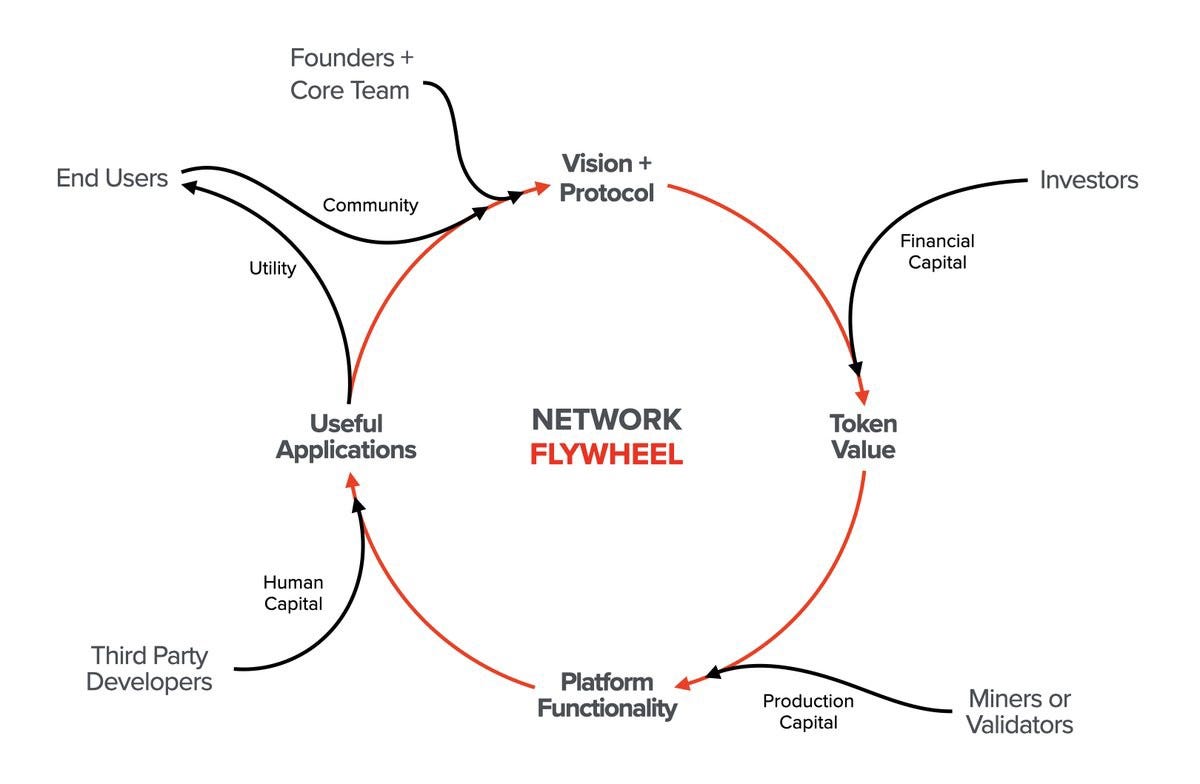

The token network flywheel as proposed by Ali Yahya here is a great example. A well-designed blockchain that has a built-in incentive structure that creates a multi-sided market with strong network effects by means of a smart native token design.

In order to recognise this value, it is important to understand this process:

The founding team communicates to the world a new vision for a decentralized network.

If the vision is compelling, a community begins to form around it

When there is demand, supply equilibrates. A core team of developers join and begin to build the protocol.

The project can bootstrap value for the network’s token as people get excited about its future usability and potential- known as the “hype phase” to many.

5. Once the protocol is complete, a different actor- miners/validators are introduced to the supply side of the network.

6. They contribute the production capital — i.e. computational resources — that give the network its functionality and security.

7. As a result of function and security, third-party developers who leverage that functionality to build useful applications on top.

8. Those applications create real-world value for end-users who drive demand for the token and, by becoming part of the community, reinforce the vision at the heart of the protocol.

9. Greater token demand leads miners/validators to have stronger incentives to support the functionality of the network which encourages developers to build Apps creating utility and a growth flywheel.

10. Once the flywheel has been set into motion, it often needs no push of its own to continue spinning. The protocol takes a life of its own as it becomes fully decentralized by its community.

Control and ownership over the blockchain protocol will then be in the hands of the token holding users, third-party developers, miners/validators, and investors who make up the protocol’s community.

If it is evident that these flywheels are in play. I implore you to take advantage of them as a builder/dev/investor. These opportunities we currently have are dated in number. When TradFi decides to finally move in, they will fill the gaps.

—

The Long Term Play

Someone’s sitting in the shade today because they planted the tree a long time ago — Warren Buffet.

As both an investor or a project founder, you need to be able to establish value. You also need to be able to constantly evaluate whether there is room for value to increase further.

To leave you with some final questions that I hope will further emphasize the importance of understanding tokenomics.

Without intrinsic value, is there any point to an investment?

If there is no speculative value, is there any point to development?

—

* If you’ve enjoyed this in any way at all, I will never ask you for any financial donations. All I ask is that you share this with your frens and give me a like on this post. Hopefully, this can serve as a guide to some more in-depth tokenomics that I haven’t heard of in any echo chambers yet.

Great Article. How about exploring the tokenomics of various protocols ? Like DeFi vs Game-Fi in an another article ?

I have been looking for an article to explain tokenomics. This served me well. Thank you